Dignity, Choice, and Accountability: Why Fiscal Intermediaries Are Essential to the Future of Home and Community-Based Care

By Tara Himmel on June 10, 2026

Contents

- Contents

- Executive Summary

- Personal Care as a Civil Right, Not a Service Category

- Common Misconceptions About Fiscal Intermediaries

- The Case for Consumer Direction: Workforce, Outcomes, and Cost

- The Role of the FI: Infrastructure for Independence

- Why Program Integrity Requires Strong FI Infrastructure

- The New York Experience: What Consolidation Delivers

- Balancing Accountability with Autonomy

- What States and Federal Policymakers Should Know

- Conclusion: The Stakes Are High

Executive Summary

For millions of Americans living with long-term disabilities, home and community-based services (HCBS) are not a benefit, they are the foundation of independent life. Consumer-directed care, in which individuals choose and manage their own caregivers, has become the defining model for delivering these services. It is cost-effective, federally authorized, and grounded in the civil rights principle that people with disabilities have the right to direct their own lives. Yet the infrastructure that makes this model function, the fiscal intermediary (FI), is poorly understood, frequently undervalued, and increasingly under scrutiny.

This paper makes the case that fiscal intermediaries are not administrative overhead. They are the architecture of accountability that enables consumer direction to work safely, at scale, and in alignment with both participant rights and public stewardship obligations.

Key Findings

- Consumer-directed care is a right, not a service option. The Centers for Medicare and Medicaid Services (CMS) and the Administration for Community Living have explicitly framed consumer direction as a civil rights issue, and it has been federally authorized across multiple Medicaid authorities.

- The direct care workforce crisis cannot be solved by agency-based models alone. Consumer direction, by enabling individuals to hire trusted caregivers including family members, produces stronger retention and higher participant satisfaction than traditional delivery models.

- FIs perform far more than payroll processing. Their functions include caregiver credentialing, background and exclusion screening, electronic visit verification, real-time payment controls, budget management, Medicaid billing, and compliance reporting, all of which are essential to program integrity.

- Some FIs already implement the structural safeguards that policy analysts recommend. These include background checks, real-time service verification, unique caregiver identification, and duplicate billing controls, often beyond current policy expectations.

- Vendor consolidation can lead to better results for participants and administrators. The consolidation of fragmented multi-vendor FI models into a single statewide FI, as demonstrated in New York’s Consumer Directed Personal Assistance Program (CDPAP), produces measurable benefits: greater data visibility, more consistent application of program controls, and the detection of fraud or waste patterns that are invisible in fragmented systems. New York’s consolidation is projected to save taxpayers upward of one billion dollars annually while providing more consistent service and benefits to participants and caregivers.

The policy question, then, is not whether consumer direction should be constrained in response to program integrity concerns. It is how states and federal policymakers can build the infrastructure that allows consumer direction to grow responsibly. The recommendations below are intended to preserve participant autonomy while strengthening the administrative, fiscal, and data controls that make consumer direction sustainable. Each reflects operational experience administering consumer-directed HCBS programs at scale and is intended to serve as a practical framework.

Recommendations

-

Procure for FI Capability, Not Just Administrative Cost. Evaluation of FI vendors should ideally be based on a defined set of capability criteria. A model procurement framework should require vendors to demonstrate the following:

- EVV technology with accessible alternatives (app and telephone)

- A rules-driven payroll engine capable of processing high timesheet volumes in near real time

- Active exclusion screening infrastructure (OIG, SSA Death Master File, state Medicaid exclusion lists)

- Unique caregiver identification enabling program-wide traceability

- Experience delivering comparable services to the same size population

- Financial capacity

- A documented compliance escalation program with defined workflows for MCO and state oversight referrals.

Contract performance standards should include fraud detection metrics, participant satisfaction scores, and payment accuracy rates — not just transactional data. Selected vendors should have demonstrated ability to provide these services at scale and with a strong history of performance. While cost is always a factor, scoring criteria that weighs low price at the expense of quality will ultimately end up costing states more. Procurement should require, at a minimum, three like-sized programs as references, and over 10 years of experience. It is important that references are available to be delivered by phone as many states prohibit written references.

-

Codify Front-End Controls as Baseline Program Standards. CMS should issue guidance establishing minimum front-end program integrity standards for all Medicaid-funded consumer-directed care programs. At minimum, these should include:

- Structured caregiver enrollment, exclusion list verification, and credentialing prior to first service

- EVV implementation with accessible alternatives

- Authorization validation before payment is processed

- Real-time spending plan enforcement

States should be required to certify compliance with these standards as a condition of federal matching funds for consumer-directed HCBS.

-

Develop a Federal Framework for FI Consolidation. CMS should develop formal guidance to support states in evaluating whether consolidation of FIs would strengthen program oversight, data visibility, and fraud detection. The guidance should include:

- Criteria for assessing when consolidation is appropriate

- A transition planning framework that protects participant continuity of care

- Technical assistance resources for states executing transitions.

New York’s consolidation of its Consumer Directed Personal Assistance Program (CDPAP), which is projected to save more than $1 billion annually without disrupting participant access, should serve as the model case study.

-

Require Person-Reported Outcomes in FI Performance Standards. Federal and state oversight frameworks should require that FI performance be evaluated on participant-reported experience alongside compliance metrics. Measures should include:

- Ease of enrollment

- Caregiver payment timeliness and accuracy

- Participant access to real-time budget information

- Customer service responsiveness

CMS’ emerging HCBS quality measure sets should explicitly include consumer direction-specific person-reported outcomes, and FI contracts should incorporate these measures as performance benchmarks.

Dignity, Choice, and Accountability: Why Fiscal Intermediaries Are Essential to the Future of Home and Community-Based Care

For individuals living with long-term disabilities, the ability to remain in their homes and communities, rather than entering a nursing facility or institutional care setting, is not a preference. It is a civil right. It is the difference between a life directed by the individual and a life managed by a system. Home and community-based services (HCBS), and particularly consumer-directed care, have become the defining delivery model for long-term services and supports in the United States. As these programs have grown in reach and complexity, the role of the fiscal intermediary (FI), the administrative backbone that makes consumer direction function, has become more critical than ever.

Yet despite broad support for and satisfaction with consumer directed care, FIs are not always well understood. They are sometimes viewed narrowly as payroll processors, or worse, as unnecessary bureaucratic layers between the consumer and their caregiver. That perception misses the reality of what FIs do, why they exist, and what happens when the infrastructure supporting these programs is absent, fragmented, or insufficient.

This conversation is happening now, and PPL is helping move it forward. As the nation’s leading FI, PPL currently supports more than 320,000 participants and 390,000 caregivers across 50 programs in 18 states, drawing on 26 years of experience administering consumer-directed programs at scale. Our rules-driven payroll engine processes over 1 million timesheets in near real time. Our compliance infrastructure screens hundreds of thousands of caregivers against federal and state exclusion lists every month. And our data systems provide state and MCO partners with the program-wide visibility they need to exercise meaningful oversight.

Federal scrutiny of Medicaid home and community-based programs has intensified, with congressional committees examining fraud, waste, and abuse in consumer-directed programs and recent policy analyses calling for structural reforms including background checks, real-time service verification, and single-vendor fiscal agent models. These proposals are well-intentioned, and, in many cases, they reflect practices that leading FIs already have in place. What is missing from the current debate is a clear-eyed, outcomes-based account of what strong FI administration actually looks like, what it delivers, and what is at stake when the infrastructure is fragmented or insufficient.

This article makes the case, grounded in federal policy, program data, and real-world experience, that consumer-direction is one of the most important and cost-effective tools in the Medicaid system, and that FIs, when structured and operated well, are the mechanism through which that model delivers on its promise of autonomy, accountability, and long-term sustainability.

Personal Care as a Civil Right, Not a Service Category

The story of home and community-based services in the United States is inseparable from the disability rights movement. For decades, individuals with physical and cognitive disabilities were institutionalized not because they required the clinical intensity of a facility, but because the infrastructure to support them in the community did not exist or was not funded. Olmstead v. L.C., the landmark 1999 Supreme Court decision, established that unjustified institutionalization constitutes discrimination under the Americans with Disabilities Act. Since then, federal policy has consistently reinforced the message: people with disabilities have the right to receive services in the most integrated setting appropriate to their needs.

Personal care, assistance with the activities of daily living such as bathing, dressing, mobility, and medication management, is the service that makes community living possible for many individuals with long-term disabilities. Without reliable, accessible personal care, remaining at home is not an option. Within the landscape of personal care delivery, consumer-directed models have emerged as not merely an alternative to agency-based care, but in many cases a superior one.

The federal government has been explicit on this point. The Centers for Medicare & Medicaid Services (CMS) and the Administration for Community Living (ACL) have jointly framed consumer direction as a civil rights issue. The HCBS Settings Rule, which established minimum standards for how and where Medicaid HCBS can be delivered, explicitly protects autonomy, dignity, freedom from coercion, and the individual’s right to choose their own providers, including in consumer-directed programs. Federal Medicaid regulation defines consumer direction as participant control over the amount, duration, scope, provider, and location of services. These are not administrative preferences. They are people’s rights.

Personal care services (PCS) was the first Medicaid service authorized for consumer direction, and it remains at the center of the model. Personal care is now available within consumer direction across multiple Medicaid authorities, including 1915(c) waivers, 1915(i) and 1915(j) state plan options, 1915(k), and standard state plan personal care, reflecting a deliberate federal policy choice to embed consumer control into the structural fabric of Medicaid long-term services and supports.

Common Misconceptions About Fiscal Intermediaries

Critics of consumer-directed programs sometimes frame it as a high-risk model, one that trades institutional oversight for individual freedom in ways that invite waste, fraud, and abuse. This framing is not only inaccurate; it gets the economics and the ethics exactly backwards.

Before examining the full scope of what fiscal intermediaries (FIs) do, it is worth directly addressing the misconceptions that most often distort the public and policy conversation about their role. These misunderstandings shape how FIs are procured, regulated, and evaluated, with real consequences for the programs and people they serve.

Misconception 1: FIs are just payroll processors.

This is perhaps the most persistent, and most consequential mischaracterization of the FI role. It is true that payroll is a core FI function. But reducing the FI to a payroll vendor is like describing a hospital as a billing department. The billing happens, but it is not the main point.

In practice, an FI is the compliance and administrative backbone of the entire consumer direction program. Before a caregiver begins serving a participant, the FI has confirmed the caregiver is who the participant chose to care for them, verified their employment eligibility, completed required documentation, screened them against federal and state exclusion lists, confirmed their background check if required by the state, and issued a unique program identifier that enables tracking across the full lifecycle of the program. Once services begin, the FI validates every timesheet against program authorizations, enforces spending plan limits in real time, monitors for billing anomalies, and generates the reporting that states and managed care organizations need to oversee the program.

None of this is payroll. All of it is essential. Evaluating FIs solely as transactional vendors is systematically undervaluing the compliance infrastructure that protects both participants and the public investment in these programs.

Misconception 2: Consumer-directed programs are more vulnerable to fraud than traditional agency-based models.

This framing appears frequently in policy discussions. The argument is that because services are delivered in private homes, by non-licensed caregivers who are often family members, traditional clinical oversight mechanisms do not apply and therefore fraud is harder to detect. This is misleading.

What this argument misses is that risk is not the same as vulnerability and vulnerability is not destiny. The presence of risk in consumer-directed programs does not mean fraud is inevitable. It means that the administrative infrastructure surrounding the program must be designed and resourced to detect and prevent it. That is precisely what strong FIs do.

Consumer-directed programs administered by capable FIs have significant structural advantages for fraud prevention. A single FI with a complete view of the program can detect billing patterns that are invisible in fragmented systems: a caregiver billing 20 hours a day across multiple participants; services claimed during a hospitalization; a participant’s death that was not reflected in billing for weeks. These anomalies are visible in aggregate data and invisible when the program is divided among dozens or hundreds of smaller vendors, each seeing only its own narrow slice of activity.

The fundamental error in the “consumer direction is more vulnerable” argument is the inaccurate assumption that fraud risk is a property of the delivery model rather than the administrative infrastructure surrounding it. Fraud follows fragmentation, opacity, and weak controls, regardless of whether services are delivered by a family caregiver in a private home or a licensed aide dispatched by an agency. Agency-based models carry their own fraud profile: inflated hours, services billed but never rendered, documentation practices designed to pass audits rather than reflect reality. These risks are not hypothetical, they are well-documented in federal and state audit findings, OIG reports, and Medicaid fraud control unit investigations. The difference between a high-integrity program and a fraud-prone one is not the type of care being delivered. It is whether the organization administering the program has the systems, data, and accountability culture to see what is happening and act on it.

The evidence from New York’s transition of its consumer direction program to a single statewide FI bears this out directly. When the program was streamlined from 600-plus FIs into one, program-wide data became available for the first time and the anomalies it revealed were both significant and previously undetectable. The question, then, is not whether consumer direction is inherently risky. It is whether the infrastructure surrounding it is strong enough to see what needs to be seen. A capable FI enables this view.

Misconception 3: More vendors means more choice for participants.

This misconception is understandable, but incomplete. It has driven fragmented FI models in states that believed a competitive marketplace of vendors would expand participant options and improve service quality. In practice, however, the number of FI vendors is not the same thing as participant choice. Choice in consumer-direction is about the participant’s ability to select, hire, train, and direct their own caregiver, not about which company provides the administrative oversight. From a participant’s perspective, the FI is largely invisible when it is functioning well. What participants experience is whether they can enroll quickly, whether their caregiver gets paid accurately and on time, whether they have real-time access to their budget, and whether someone is available to help when they have a problem. These are outcomes determined by the quality and capability of the FI, not by the number of FIs competing in the market.

Models in which dozens or hundreds of FIs operate in the same program do not improve the participant experience. They fragment data, create inconsistent program administration, reduce accountability, and eliminate the economies of scale that enable investment in technology, compliance infrastructure, and customer service. When the FI market is crowded with small or undercapitalized vendors, the participants most likely to suffer are those with the most complex needs: individuals who require the most administrative support, encounter problems most frequently, and are least equipped to navigate a vendor landscape that was never designed with them in mind.

True choice in consumer-directed programs is best protected not by multiplying the number of administrative intermediaries, but by ensuring that the FI administering the program is capable, accountable, and genuinely focused on the participant’s ability to direct their own care. More vendors does not mean more choice. It means more fragmentation and fragmentation, as the data consistently shows, is where fraud hides and participants fall through the cracks.

A single, accountable FI does not constrain participant choice, it protects and enables it. When one organization is responsible for the entire participant experience, there is no ambiguity about who is accountable when something goes wrong, no fragmented data obscuring the full picture, and no gaps between vendors for participants to fall through.

Accountability at scale also creates the capacity to invest where it matters most: in the communities where participants live. PPL operates with a multilingual, culturally competent team embedded across the communities we serve. Participants can access support in their own language, from staff who understand their cultural context and the realities of their daily lives. This is not a call center model. It is community presence backed by the infrastructure and accountability that only a statewide FI can provide

In this model, scale and community are not competing values, nor are statewide accountability and local partnerships.

This is PPL’s model. It does not reduce choice. It delivers it.

The Case for Consumer Direction: Workforce, Outcomes, and Cost

Consumer direction solves a workforce problem that traditional models cannot.

The direct care workforce crisis is among the most acute challenges facing the American healthcare system. According to data from the Paraprofessional Healthcare Institute (PHI) and the Bureau of Labor Statistics, annual turnover rates in agency-based home care often exceed 60% and surpass 80% in some markets, making workforce stability one of the most persistent challenges in the sector. (PHI. Direct Care Workforce Chartbook. phinational.org). Low wages, difficult conditions, and limited flexibility make recruitment and retention persistently difficult. The consequences are felt directly by people with disabilities, who face service gaps, caregiver instability, and in some cases, avoidable hospitalizations or facility placements.

Consumer-directed models address this crisis in ways agency-based care cannot. When individuals are empowered to hire, train, and supervise their own caregivers, including trusted family members where permitted, they are better able to build stable, long-term care relationships. Additionally, FIs are able to provide more comprehensive benefits to caregivers when operating at scale. CMS, ACL, and MACPAC (the congressional advisory body on Medicaid) have all explicitly linked consumer direction to workforce stabilization. Federal guidance encourages states to use payment increases, wage pass-throughs, and consumer direction to strengthen caregiver retention.

The scale that the single FI model affords also makes it possible to support caregivers in a way that professionalizes their role through streamlined, reliable payroll processing, fair and equitable wages, and access to benefits that meet their needs. This type of support matters enormously for workforce stability and is typically unfeasible in fragmented, multi-vendor environments. Caregivers who experience this level of consistency and stability are more likely to remain in their roles, invest in their relationships with participants, and treat direct care as a career rather than a temporary arrangement. PPL has demonstrated that this is achievable at scale, and that it directly strengthens the quality and continuity of care for participants.

Evidence from comparative studies and systematic reviews indicate that consumer-directed models are associated with higher participant satisfaction and improved caregiver outcomes, including greater intention to continue caregiving, relative to traditional agency-based delivery.

Consumer direction produces better outcomes at lower cost.

Consumer-directed programs allows individuals to tailor their care to their actual lives, not to the schedules or staffing constraints of an agency. Participants who direct their own care report higher levels of satisfaction, greater sense of control over daily routines, and stronger connections to their communities. These are not soft metrics. They reflect the core purpose of long-term services and supports: to enable people with disabilities to live full, self-determined lives.

From a cost perspective, HCBS, particularly consumer-directed models, represents a fiscally responsible alternative to institutional care. Nursing facility care can cost three to four times more per person per year than community-based alternatives. Federal and state policymakers have increasingly recognized that supporting people in their homes is not only the right thing to do; it is the economically sound thing to do. New York’s CDPAP program, for example, has supported hundreds of thousands of consumers in directing their own care in the community, at a fraction of the cost of the institutional alternative.

The conclusion drawn by CMS, ACL, and MACPAC is consistent and clear: consumer direction is not a niche option at the margins of HCBS. It is a central, scalable, and essential component of a sustainable long-term care system.

The Role of the FI: Infrastructure for Independence

An FI, when operating at scale with the right infrastructure, is not a middleman. It is the architecture of the program itself: the system through which participant rights are operationalized, caregiver compliance is enforced, Medicaid dollars are protected, and state oversight is made possible. Critics who characterize FIs as administrative intermediaries miss the fundamental question: not whether an FI exists in the chain, but whether it has the scale, capability, and organizational commitment to transcend the transactional aspects of the role.

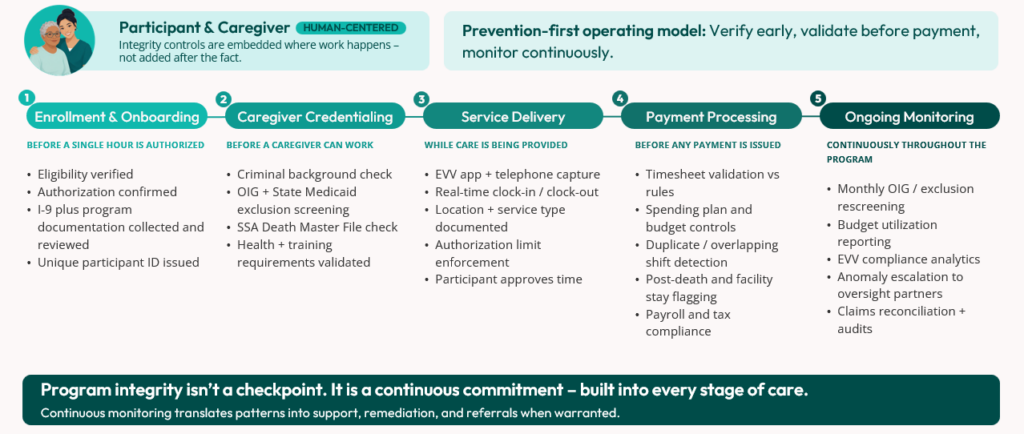

At its most fundamental level, an FI exists to remove administrative burden from participants and their caregivers so that participants can focus entirely on directing their care. In every consumer-directed program, the FI processes payroll and remits payroll taxes on behalf of the Medicaid participant, who is the legal employer of their caregiver in most programs. This requires precision, regulatory expertise, and systems capable of handling complex federal and state tax requirements, caregiver credentialing, service verification, and Medicaid billing simultaneously and at scale.

Understanding what FIs actually do, and what happens when they are absent, disparate, or undercapitalized, is essential to any honest conversation about program integrity in consumer-directed HCBS.

But the FI’s role extends well beyond payroll. Across programs nationwide, they provide:

- Enrollment and credentialing. Before a caregiver can provide a single hour of care, the FI ensures they have completed required documentation, including I-9 employment verification, and other program eligibility requirements, including background checks where required by the state. The FI also confirms that caregivers have been screened against federal and state exclusion lists, including the OIG List of Excluded Individuals/Entities and the Social Security Administration Death Master File. These standard processes are the first line of defense against ineligible or fraudulent actors entering the program.

- Electronic Visit Verification (EVV). Federal law now requires EVV for personal care services, and FIs are central to its implementation and enforcement. A well-designed EVV system captures the service type, the individual receiving care, the caregiver providing it, the location, and the start and end times of every visit, which provides real-time confirmation that authorized services are being delivered as planned. For participants with limited technology access, telephone-based, dial-in EVV systems ensure that the accessibility needs of the consumer-directed population are met without sacrificing program integrity.

- Real-time work controls. Submitted time is reviewed through automated program controls before it advances through the payment workflow. These controls operate at scale and in near real time, comparing each submission against available authorization, enrollment, eligibility, EVV, and spending plan information. For example: Does the participant have an active authorization to receive the service? Has the caregiver completed required enrollment and clearance steps? Does the time submission align with the approved service authorization, budget, and applicable program rules? When a submission does not pass these controls, the item is flagged for review, correction, or escalation in accordance with program procedures. This allows timely outreach to the participant, designated representative, caregiver, MCO, or state partner, as appropriate, to resolve documentation, authorization, or data issues while supporting accurate program administration and compliant claims submission.

- Budget management and transparency. FIs provide participants and their designated representatives with real-time visibility into their authorized budgets, expenditures, and remaining balances. This transparency supports informed decision-making, prevents overspending, and ensures that Medicaid dollars are deployed in accordance with approved plans.

- Reporting and oversight. FIs generate the data that states and MCOs need to monitor program health, identify anomalies, and make informed policy decisions. From budget utilization reports to EVV compliance analytics, this reporting infrastructure is essential to responsible program stewardship.

- Medicaid billing. Unlike traditional healthcare providers, caregivers in consumer-directed programs are not assigned National Provider Identifiers (NPIs) as they are not HIPAA-covered clinical providers. A unique caregiver ID from a statewide FI allows validation of time submitted across the program for each individual caregiver. The FI then submits Medicaid claims on behalf of the program, ensuring that billing is accurate, timely, and compliant with federal and state requirements.

In short, the FI is not a middleman. It is the administrative and compliance infrastructure that makes consumer direction safe, scalable, and sustainable for large statewide programs.

Why Program Integrity Requires Strong FI Infrastructure

The conversation about fraud, waste, and abuse in HCBS has understandably grown louder in recent years. Home and community-based programs, particularly those involving personal care, present real program integrity challenges if the appropriate oversight is not in place. The personal, often home-based nature of these programs necessitates a thoughtful, layered approach to program integrity; one that does not undermine the autonomy and accessibility that make consumer direction valuable, but that embeds strong controls at every stage of the program lifecycle.

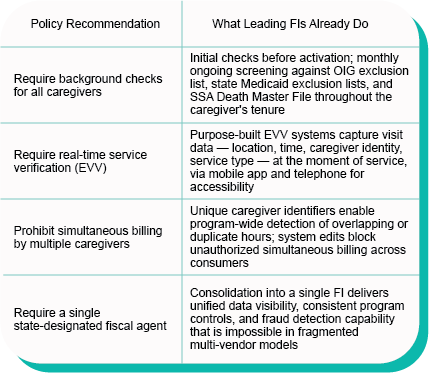

Some recent policy analyses have characterized consumer-directed services as “especially vulnerable” to fraud and abuse, and have proposed structural reforms including required background checks, real-time service verification, and the use of a single fiscal agent. These recommendations are well-grounded. But what is sometimes missing from this conversation is the recognition that some FIs, such as PPL, already implement these practices as standard operating procedure. FIs that have made these investments are also well situated to serve as a bridge for needed reform, translating their own operational insight and experience into programmatic improvements while having the unique ability to collaborate and execute on those identified at the broader system level.

Consider the alignment between best-practice policy recommendations and what strong FI-run programs actually do:

- Require exclusion list checks for all caregivers. The practice: A rigorous FI conducts initial checks before activation, screens against multiple federal and state exclusion lists, and performs monthly ongoing screenings throughout the caregiver’s tenure — ensuring that a caregiver who was eligible at enrollment does not remain active after a disqualifying event.

- Require real-time service verification. The practice: FIs with purpose-built EVV systems capture visit data at the moment of service (including location, time, caregiver identity, and service type) through mobile applications and telephone systems designed for the accessibility needs of the consumer-directed population.

- Prohibit simultaneous billing by multiple caregivers for the same hours. The practice: Well-designed FI systems assign unique identifiers to every caregiver, enabling program-wide detection of overlapping or duplicate hours across all consumers and plans. System edits prevent a caregiver from submitting time for multiple consumers simultaneously unless a specific, authorized service code is in place.

- Require a single state-designated fiscal agent. The practice: The consolidation of fragmented multi-vendor models into a single FI is one of the most powerful program integrity tools available to states — and the evidence from New York is instructive.

The results of strong FI administration are measurable. In New York’s CDPAP program (now administered by a single statewide FI), a survey of nearly 95,000 participants found overall satisfaction with PPL, the statewide FI, averaging 4.31 out of 5, up from 4.04 in May 2025. Timekeeping satisfaction rose to 4.39 out of 5. Projected annual savings exceed $1 billion. These are not incidental outcomes. They are the direct result of investing in the infrastructure that makes consumer direction work at scale, with accountability, and without disrupting participant access.

The New York Experience: What Consolidation Delivers

To understand what New York’s consolidation achieved, it helps to understand what it replaced. Prior to 2025, CDPAP operated across more than 600 FIs of varying size, capability, and administrative sophistication. Enrollment processes, credentialing standards, and billing practices varied widely from one vendor to the next. Data was siloed, making it impossible for the state or MCOs to identify patterns across the program as a whole. Some intermediaries lacked the technology infrastructure to implement EVV effectively. Others operated without the compliance resources to identify or escalate suspected fraud, waste or abuse. The result was a fragmented system in which improper payments were structurally difficult to prevent.

In 2025, New York undertook one of the most significant structural reforms in the history of its Consumer Directed Personal Assistance Program (CDPAP) and initiated one of the largest-ever Medicaid program transitions, consolidating a program that had operated across more than 600 entities into a single, statewide FI. The results have been striking.

With a unified view of the program rather than hundreds of data silos, for the first time it became possible to identify patterns that simply could not be seen when data was disparate. Caregivers billing excessive hours across multiple participants. Attempted billing after a participant’s death. Services claimed during facility stays. Overlapping shifts that were invisible when each FI could only see its own slice of the program.

Within months of consolidation, proactive analytics on caregiver behavior identified suspicious patterns that were escalated to the state and MCO partners for investigation. Program reforms implemented through the transition identified and eliminated improper payments that had gone undetected in the previous system. All in all, they were projected to save New York taxpayers upward of one billion dollars annually.

In a 2026 survey of nearly 95,000 CDPAP participants, respondents rated their overall satisfaction with the transition an average of 4.31 out of 5, up from 4.04 out of 5 in a previous May 2025 survey. Similarly, satisfaction with PPL’s timekeeping systems increased to 4.39 out of 5, up from 4.27 out of 5 in May 2025. And finally, respondents consistently praised PPL’s Time4Care mobile app, ease of clocking in and out, and improved visibility into hours and authorizations compared to prior fiscal intermediaries.

The transition demonstrated the power of scale applied to program integrity. A single FI with a complete view of the program can do what no collection of smaller vendors can: identify anomalies that only become visible in aggregate, enforce rules consistently across every consumer and plan, and generate the data that state agencies need to exercise meaningful oversight.

The lesson is not that consolidation is appropriate in every state or program. Program design varies enormously, and the right structure depends on the size, complexity, and policy goals of each state. But the New York experience makes a compelling case that strong, centralized FI administration, paired with robust compliance infrastructure, is among the most effective tools available for protecting program integrity while preserving participant access.

Balancing Accountability with Autonomy

One of the most important (and sometimes underappreciated) aspects of responsible FI administration is the recognition that program integrity and participant autonomy are not in tension. They are complementary.

Federal policy has been clear on this point. CMS guidance emphasizes risk mitigation without eroding consumer authority. Oversight is framed as enabling consumer direction, not policing it. The goal is shared responsibility: participants retain control over who provides their care and how it is delivered, while the FI and the state ensure that the administrative infrastructure surrounding those choices is sound.

This means that program integrity controls must be designed with the participant at the center, so that even measures like background checks and exclusion screenings function as harm reduction and not barriers to access. EVV systems that include telephone options ensure that individuals who cannot use smartphones are not excluded from the program. Budget transparency tools empower participants to make informed decisions about their own care. These are not compliance burdens. They are features of a program that respects its participants.

The quality of consumer-directed HCBS, as federal policy increasingly recognizes, is measured not solely by compliance metrics but rather by the lived experience of the people the program serves: their sense of autonomy, their participation in community life, their ability to shape their own daily routines. New quality measure frameworks being developed by CMS and MACPAC emphasize person-reported outcomes alongside traditional compliance indicators, reflecting a shift in how the federal government thinks about what “quality” means in HCBS.

A well-run FI contributes to quality on both dimensions. By handling the administrative complexity of the program reliably and accurately, the FI frees participants and their designated representatives to focus on what matters most: building stable care relationships, managing their health, and living fully in their communities.

What States and Federal Policymakers Should Know

As federal and state policymakers continue to shape the future of HCBS by navigating budget pressures, workforce challenges, and the ongoing imperative to reduce fraud, waste, and abuse, several principles emerge from the experience of leading FIs that are worth keeping in mind.

- Consolidation strengthens oversight. Programs with a single or limited number of FIs have greater data visibility, more consistent application of program controls, and stronger capacity for fraud detection than fragmented multi-vendor models. Where appropriate, consolidation is one of the most effective structural reforms available.

- Front-end controls prevent back-end problems. The most efficient fraud prevention happens before services begin, through enrollment screening, caregiver credentialing, authorization validation, and spending plan controls. Investing in robust onboarding infrastructure reduces the need for costly post-payment recovery.

- Scale creates capability. A national FI with hundreds of thousands of caregivers across dozens of programs can detect patterns and anomalies that are invisible at a smaller scale. National data creates the ability to see what no individual state program can see on its own, and to share best practices, insights, and early warning signals across the system.

- Integrity and access are not competing values. Well-designed program integrity infrastructure protects participants, strengthens programs, and builds public trust, without restricting access or undermining the autonomy that makes consumer direction valuable. Policymakers should resist frameworks that treat these as trade-offs.

Conclusion: The Stakes Are High

Millions of Americans are enrolled in Medicaid HCBS programs, with millions more on waiting lists. An aging population and a strained direct care workforce mean that pressure on these systems will only grow. The decisions made now about how to administer these programs, who administers them, and the standards to which they are held, will shape the lives of people with disabilities and older adults for decades to come.

FIs ensure that the right people receive authorized services, that caregivers are properly credentialed and compensated, that Medicaid dollars are spent appropriately, and that the data exists to identify problems and drive continuous improvement.

Done well, this work changes lives. The person with a spinal cord injury who can hire a trusted neighbor or family member as their own caregiver and direct their own daily routine is not just receiving a service. They are exercising a right, living a life of their choosing, and participating in their community on their own terms. The FI, working quietly in the background, is what makes that possible.